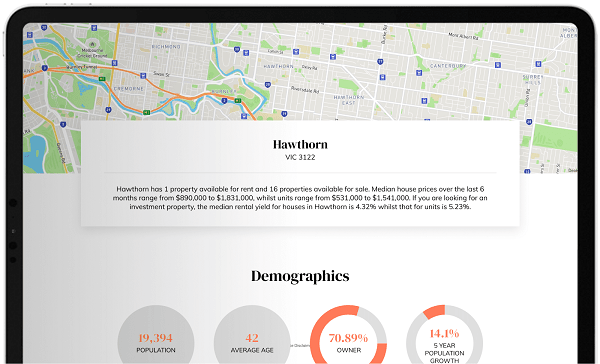

7 investment properties, all designed for maximum return.

Real Estate is the ultimate passion. When I grew up in East Keilor my parents went through 3 extensions. They bought the classic 14sq AV Jennings home. They put on the rumpus, they then went upstairs a few year later and then did the pool and garage a year or two later.

I as a younger chap then, I loved chatting to the tradies and I now know, that tradies are one of your biggest assets in building a real estate portfolio. Mum and Dad added value to their home all the way through, but never invested outside of their principle place of residence, which was both a generational and ancestry mindset.

At school, I studied economics, legal studies and accounting in HSC. Then I went on to qualify as an accountant where I was a tax agent before working in Superannuation at Colonial Mutual.

I saw first hand what returns people received in both investment and superannuation funds back in the early to mid 90’s. Mind you, it was the early 1990’s, so it was hard to get a lot of growth due to Paul Keating’s “Recession we had to have”. And Paul was right, there was no way out of the inflation spike back then, interest rates had to rise and it hurt many people, particularly the Pyramid Building collapse

Back to East Keilor, when Mum and Dad went through these home improvements I was often the one doing them. I painted, sanded, cut, paved and laboured. But what I also had was a fascination about was the floorplan of the home. Being a 14 sq home with 2 extensions, I found myself trying sketching a way to put is more space and less corridors or hallways and adding value. I was 17 at the time. I finished year 12, got into VUT University, but took 12 months off and then went back and studied accounting. In that time I did my real estate sub agent course in 1991 as I was interested in real estate. My two sisters who were older, were buying land and renovating homes in Sunshine at the time. So I always had this real estate thing that was always stuck in my head. After 2 years in superannuation I then got into real estate after a short stint at Qantas, I worked for 3 years as a fresh 23 year old in Essendon and I had a niche where I could sell flats and unrenovated. properties as I knew the value that could be created to these homes.

After developing my passion in real estate and seeing many succeed in investing in it, my wife and I bought in 1998 for $180k and sold for $468k after a 2 year reno. Then we bought for $315k and sold for $440k after a modest $15k reno. The reason for selling these homes was due to the home being a principle place of residence meaning the gains are 100% tax free plus we had too much equity in them meaning they were geared for tax depreciation. We then bought out family home in 2003, we bought on a big enough block in a great street. I have learnt there are two main reasons people sell their homes, no room to improve or don’t like the location. We renovated and extended it over a 5 year period and still to this day we live there. Over the 5 years renovating we invested in shares rather than real estate and we encountered the GFC in 2008 but we didn’t sell until we recouped the losses some 10 years later. We are still in shares today but we use the 30% rule and mainly invest in value shares but we also have a few growth stocks. In 2010 we entered property investment, I purposely didn’t want to follow in my parents footsteps and only have the one property. I admired all the European settlers in Australia and their mindset for real estate, they all knew something Australian ancestors didn’t know and that is that land is not getting made anymore. When choosing the properties to buy we wanted ensure it was close by to us, so we could easily add value to it that way. Our first was in Tullamarine, it’s 19kms from the City and so is Oakleigh but Tullamarine has a median house price of $760 whereas Oakleigh is $1.4M. I figured I could add value. We rented the 3 bedroom weatherboard for 4 years and then knocked down and built 2 townhouses and a unit at the back on the site. Again in 2016 we bought another weatherboard but this time in Sunbury and knocked down and built two townhouses, and then again in 2018 another weatherboard and knocked down and 2 townhouses built just recently.

My 5 tips for investing in real estate. There are many more than 5 things to consider, but this is all we have time for.

- From an property investment point of view, the cost of stamp duty and capital gains tax should prevent you for selling real estate. Rather than trading real estate think about adding value. If you are inclined to want to trade real estate perhaps you are best to consider trading shares.

- Real Estate is not a passive investment. It’s not a set and forget. Real estate is a hands on investment vehicle and those that engage that way will always succeed the most. Always look to add value, don’t be afraid to DIY, if you can make the time, but always use trades for the more technical work. Adding value is building equity which assists with purchasing power on the next property and unlocks cash.

- Chose wisely when choosing how to structure ownership, whether that be a family trust ( note you need a family for this to be effective in offsetting income ). When considering tenants in common, consider its borrowing limitations down the track, but yes it allows you to borrow cheaply and claim tax depreciation against your personal income. Get advice from an “Accountant” or Financial Adviser that has good tax and superannuation knowledge.

- Have a relationship with your banker. Create a relationship with the bank even though you might use a broker. Moving banks is hard work, and a relationship with a bank can help ensure you stay on the best rates and get approvals on your next project. Also consider utilising the free the bank valuation service, that is usually available every 12 months, this is particularly important if you are adding value. The banks knowing your LVR or what I like to call it your loan health is important as they like good debt and get regulated on this. Also ensure you pay all your bills on time. Banks receive your credit scores whenever you apply for credit and although this doesn’t have an impact on your existing loan it will have an big impact on future borrowing.

- Lastly, keep the Taxation Office, the Council and State Revenue office honest. Ensure you have a depreciation schedule, to claim the full depreciation you need a qualified Quantity Surveyor and Tax Accountant. People think they don’t need a quantity survey, they are wrong, I have used a quantity survey every time and they make it worthwhile every time, even if the home is 30 years old they find depreciation. As a minimum you should ensure you have an understanding on what a repair is versus what constitutes a replacement and how that effects your yearly deductions and depreciation. Ensure you review your Notice of Assessment on your rates from your council. Councils are capped at a 2% increase for rates but that applies across all properties, so councils can increase the rates by 2% but the value taxed can increase by a lot more and is determined by the valuation they provide. For example the CIV is the amount you pay rates on, look at this amount and compare it to last year and work out if your increase is higher than the market. A good real estate agent can help you here. Likewise with the Site Value on the assessment notice from council, this value actually goes to the State Revenue office which determines your Land Tax. Again you are in your right to object if the value has increased above other recent comparable sales or the median home price over the last 12 months.

And lastly, if I could add one more tip, seek out advice from professionals and not friends, I find friends are armchair experts, they mean well but they don’t your your financial health or goals. An example on where you are get free professional advice is via your Superannuation fund, they usually offers you a 1 hour free consultation each year with a financial planner. Real estate investing is tax effective but so is superannuation and if your nearing retirement you should find out how you real estate investments might impact on your retirement.

OBrien Real Estate recommends the following corporate partners:

– Quantity Surveying – Mitchell Brandtman Jennie Jeon jjeon@mitbrand.com or www.mitbrand.com More information can be found here: https://obriendashboard.com.au/images/mitchell_brandtman_tax_depreciation_schedule_offer_updated_2022.pdf

– National Australia Bank – Australia’s only bank that doesn’t offshore jobs and has the highest Net Promoter Score of all Banks. https://www.nab.com.au/

– H & R Block Taxation Accountants. https://www.hrblock.com.au/

– RentCover insurance for Rental Providers. 1800 661 662 or https://www.rentcover.com.au/

Article written by Jason Mudford