How To Finance A Home Renovation

6 Ways to funding a house reno

Thinking of renovating your home? Firstly, you should have a plan as most renovation projects take time, energy and cost money. We have listed six ways you can finance your house renovation project.

If the renovation is an extension to your home or a kitchen refit your best bet is have the plans drawn up. Then get at least 4 quotes if you have to engage the services of a professional builder. This will make it much easier for the lender when trying to give you approval.

There are multiple options that can suit your “dream”. We have listed 6 below that may help you with funding your renovation.

Handy Tip

Before you begin bear in mind that if you increase your loan amount the amount of interst you have to repay will increase. Make sure you budget for this.

1. Equity in your home loan

What is Equity? Equity is the difference between the bank’s valuation of your house and the amount you owe on the loan.

When it comes to renovating people will typically dip into the equity that is available in their home loan. The formula lenders use is the current value of your home prior to any renovstions being caqrried out. So the first test you must do is calculate the cost of the renovations. If the reno costs are lower than the equity you have avalable to you then you can talk to your lender. The NAB has a useful Equity Calculator that can estimate the amount you can potentially borrow.

2 Construction loan

A constuction loan is very much like a home equity loan as mentioned in Point 1. The difference is that the lender will value you the property after the renovations are completed. The lender will not loan the total amount upfront, The lender will stagger their lonas as the project moves forward. Paying each bill as it comes in means you don’t pay interest on your building costs until work’s actually been done. This give you better cash flow.

3 Line of credit

This may be the least popular ways of financing your home renovation. It’s basically a credit card type facility with a higher interest rate, and only has interest only repayments. Interest is only paid on the money you use, and as you pay down your balance, you can continually re-borrow the funds without going through the hassle of reapplying.

You can get the same benefit from doing a home equity loan as per Point 1, but on a lower rate. Care must be taken not to get in over your head in terms of serviceability. Make sure you can make repayments on the line of credit that will reduce the principle.

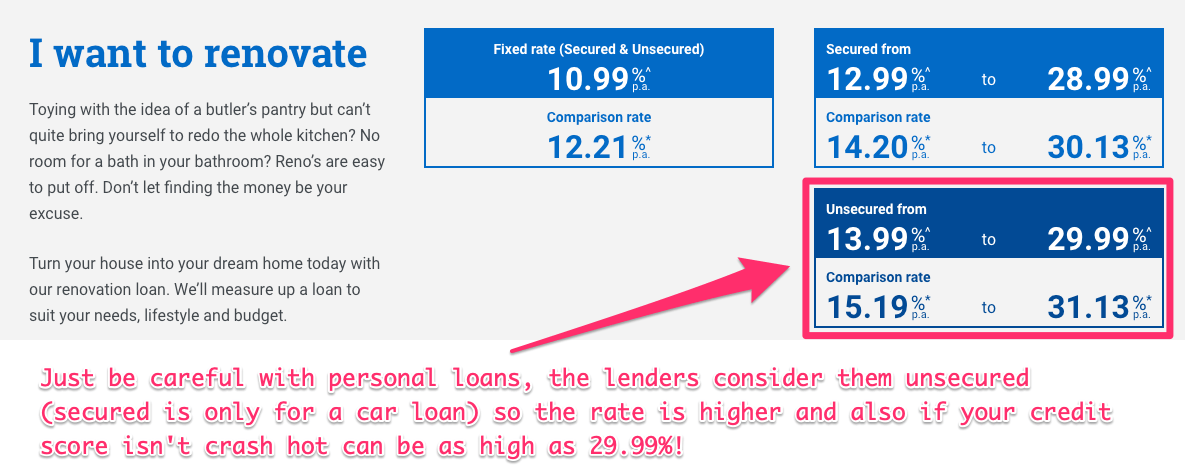

4 Personal loan

If you’re only making minor or cosmetic renovations then a renovation personal loan is all you may require. Personal loans are usually set up to $30,000, but interest rates on personal loans are higher than on home equity loans.

5 Homeowner mortgage

If you’re planning to completely transform your home and undergo a major makeover, this may be a good option as you can spread the cost over a long period of time. You could even possibly borrow up to 90 per cent of the value of your home and take advantage of mortgage rates, which are often lower than credit card and personal loan rates.

6 Credit cards

If the amount of money you are going to spend on your renovation is minimal then a credit card could be a good option. However interest rates are a lot higher for credit cards compared to standard mortgage rates. The interest on a credit card can be 21.45%.

Why could a credit card be beneficail to paying for your renovation? There are many guides that suggest the credit card is the way to go. But i suggest you exhaust all avenues avaliable to you before deciding. The credit card option is for very small reno projects. As mentioned the interest rates are much higher but if the cost of renovating is small this could be less than the estashblishment fees on other types of loans.