Monthly Property News 9th Edition 2025.

“August Market Update – Victoria’s market at a glance”

Hi everyone, I’m Jason Mudford from OBrien Real Estate with the August property news for 2025, a fast wrap on prices, stock, rentals and sentiment across metropolitan Melbourne and Regional Victoria.

Melbourne homes values rose +0.3% in August as reported by Cotality’s Home Value Index. The depth of buyers in the market continues to improve with borrowing capacity improving on the back of recent cash‑rate cuts. We’re seeing stronger activity at opens and healthy bidder numbers in well‑priced campaigns. Buyers remain price sensitive above the guide, but A‑grade listings are still attracting multiple interested parties.

The total available stock on market remains below average; July’s Melbourne new listings are off 9.4% year on year according to realestate.com.au. Expect a spring lift to improve choice without materially weakening conditions.

Auction result clearance through to late August tracked around the low–mid 70s, with inner‑metro pockets consistently outperforming. Vendor discounting has narrowed for locations and dwelling types where competition is at its deepest.

Regional Victoria values rose 0.6% over August. Conditions vary by corridor: Geelong’s family suburbs are holding firm; Ballarat remains value‑driven; Bendigo and Latrobe Valley are steady; and the Surf Coast has normalised from pandemic peaks.

National rental vacancy is sitting at 1.2% and at 1.8% for Melbourne. Annual rent growth on Cotality’s index has Melbourne at +1.2% and Regional Vic at +4.2% growth. Gross yields are 3.7% for Melbourne dwellings and 4.3% for Regional.

With Melbourne recording the softest rental market Nationally, rental providers should price with precision and consider minor value‑add upgrades to reduce days‑to‑let; renters face competitive opens in well‑served suburbs but may find relief in adjacent pockets just beyond the hot spots.

Buyer enquiry has lifted in the weeks since the RBA cut rates in August, particularly among upgraders and first‑home buyers seeking pre‑approvals ahead of spring. Dwelling approvals remain below long-term averages, building commencements have been constrained by finance and labour availability. The forward pipeline suggests a further lag in completions into 2026, which should keep the market relatively supply‑constrained through the next phase of the cycle.

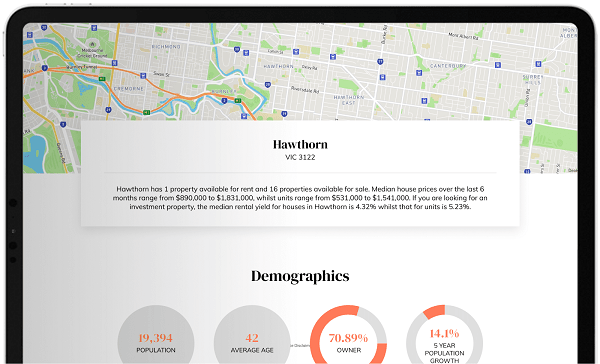

- Free Sales Price Report: https://www.obrienrealestate.com.au/property-report/

- Free Rental Report: https://www.obrienrealestate.com.au/rental-report/

- View our Annual Axis Report: https://www.obrienrealestate.com.au/axis/

Check out our website for:

Scheduled Auctions

This Week’s Opens

Our Suburb Reports