Buying Land To Build On

The positives of buying land and building a house

1. What are the advantages of buying land and building?

If you do your homework and get solid advice then building on the land you buy can be rewarding and profitable. Firstly, you can choose the design the home or choose from multiple layouts and live in an area you are comfortable in. Secondly, you can move into your home that is brand new.

There are many advantages to buying a parcel of land and building your own home. Purchasing land in an area that caters to schooling, shopping and leisure can appreciate markedly over time. Depending on your situation you may also be eligible for Government Home Grants.

As the build progresses you pay as you go. This is typically done in stages. The first stage being the purchase of the land. Then the completion of the floor followed by the roof, the lockup and finally the completion. So it is important to tailor your loan to suit these stages. This way you are under no obligation to pay the entire loan until all stages are complete.

Prior to making any commitment be aware of your loan agreement and the contract with the builder. Ask others who have gone down this path for advice. Go to forums and see how they rate their lender and builder. There is a mountain of information on the internet that can answer most questions and fears you have. Do your homework!

2. How to choose a block of land?

Make a list of requirements that will suit your lifestyle in the suburb and region.

The ideal scenario for any person or couple when buying land and building is being comfortable in the community. Common requirements are day care facilities, schools, shopping precincts, public transport and communal groups such as sporting clubs. Here is a broad list of requirements that can look for.

Services – What are your needs? Do you require childcare, schooling, medical facilities and public transport? If all these services are available then great. If not check with the local council and see what their plans are going forward.

Zoning – What is the council zoning for the suburb? Is the area only zone residential? Or, are there plans to incorporate commercial areas in the future? These are factors that can determine the value of your property as time passes. Find out if the area is targetted as a high-density population. Your suburb may look ideal in the beginning but the general makeup of the area can change dramatically over time. Enquire as to the possibility of sub-division of your land. Find out if you can add an extra dwelling such as a granny flat on your property.

The topography of your block – If your block is flat and without vegetation then there should be no expenses in relation to excavation and tree removal.

However, the removal of trees can cost you a lot of money. And are you able to remove all of the trees? You will need to see if there are any restrictions. If your block of land is on a slope then levelling the block will come at a price. Also, are there rocks on the property? If so, this adds more costs to your construction.

If your property is located in a high fire risk area then expect your insurance to be higher. This also includes the possibility of flooding. Once again add these questions onto your checklist.

3. Do I have to pay stamp duty?

You will pay Stamp Duty when you purchase the land. The build can commence construction when settlement is in place and the land is in your name. The ideal situation is to make a settlement happen when the building plans have been approved by the council. This contributes to minimising your borrowing fees.

However, you can choose to make one final payment to the builder after completion. In this case, the builder will buy the land and cover all building costs. The builder is paid once your loan comes into effect.

In this scenario, you will have to pay stamp duty on the full purchase price of your land and house. Other expenses will include stamp duty and solicitor’s fees on the land purchased. The builder’s loan costs including interest and fees. And finally, the construction costs.

4. Am I eligible for the First Home Owner Grant?

Here are some instances on how most state governments tend to subsidise those buyers buying a new home over an established one. In NSW the $7,000 First Home Owner Grant was discontinued in 2012, and there is now a $10,000 First Home Owner Grant for new homes available.

If you’re not a first-time buyer, you can still get a $5,000 grant for new homes – which means even if, for example, you’re after self-employed home loans for your second property, you can still benefit.

Similarly, in Queensland, the $15,000 Great Start Grant helps those buying or building a brand new home, while the Australian Capital Territory only targets new or renovated properties with its $12,500 grant.

If you are buying or building a new home in Victoria valued up to $750,000, you may be eligible for a First Home Owner Grant (FHOG). If you are eligible for the FHOG and the home you are buying is in regional Victoria, you will receive $20,000. If the home is not in regional Victoria, the grant is $10,000. The home must be less than five years old to be eligible for the FHOG.

First Home Owner Grant Information in each state of Australia

Australian Capital Territory

NSW

Northern Territory

Queensland

South Australia

Tasmania

Victoria

Western Australia

5. Who is the best land and construction lender?

You can start with banks and mortgage brokers. Also, you may want to consider the advice of a mortgage manager.

Some of the best advice will come from people who have already gone down the path of buying land and building their home on it. Or you may want to join a forum such as Home Renovation and Building Forum. There are literally thousands of topics that discuss all types of questions and experiences people have had when buying land and building.

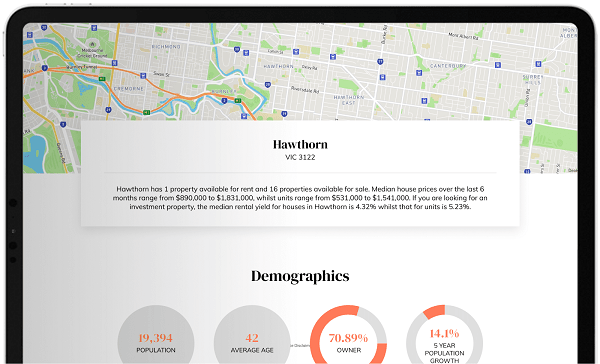

Browse our list of land sales throughout Melbourne.